Today’s jobs report was a glaring indication that the job market is weakening. On one hand, wage growth was faster than expected; on the other hand, top line jobs numbers missed estimates for the first time since April and the second time this year after months of job growth that far exceeded expectations, and jobs numbers from the past two months were revised down by 110,000, the worst downward revision since April and the second downward revision of more than 100,000 jobs since the beginning of the year.

The increase in large downward revisions is revealing: it shows that the current job market may not be as strong as many analysts said it was.

And yet, stocks were relatively muted amidst the job market’s cooldown. This is despite the fact that the Fed remains poised to increase interest rates by 25 basis points during its July meeting, and the weakening employment situation over the past few months raises questions about whether the job market may be beginning to buckle under the continued pressure of elevated interest rates.

This is the exact opposite of what happened yesterday, when ADP’s forecast of nearly 500,000 new jobs in June left investors worried about continued strength in the job market leading the Fed to leave interest rates elevated for longer.

This is also in contrast to last month’s job report that saw job growth at nearly double the forecasted pace and sent markets soaring.

It seems that markets have shifted once more from worrying about the job market’s strength to worrying about rising interest rates. The focus on interest rates tends to produce bizarre phenomena: markets would react positively to weaker or mediocre job reports and negatively to stronger job reports. This phenomenon was especially evident when aggressive rate hikes struck fear into the hearts of investors over the past year. The relationship went back to normal as the Fed gradually slowed down rate hikes, but has inversed again as of today’s job report.

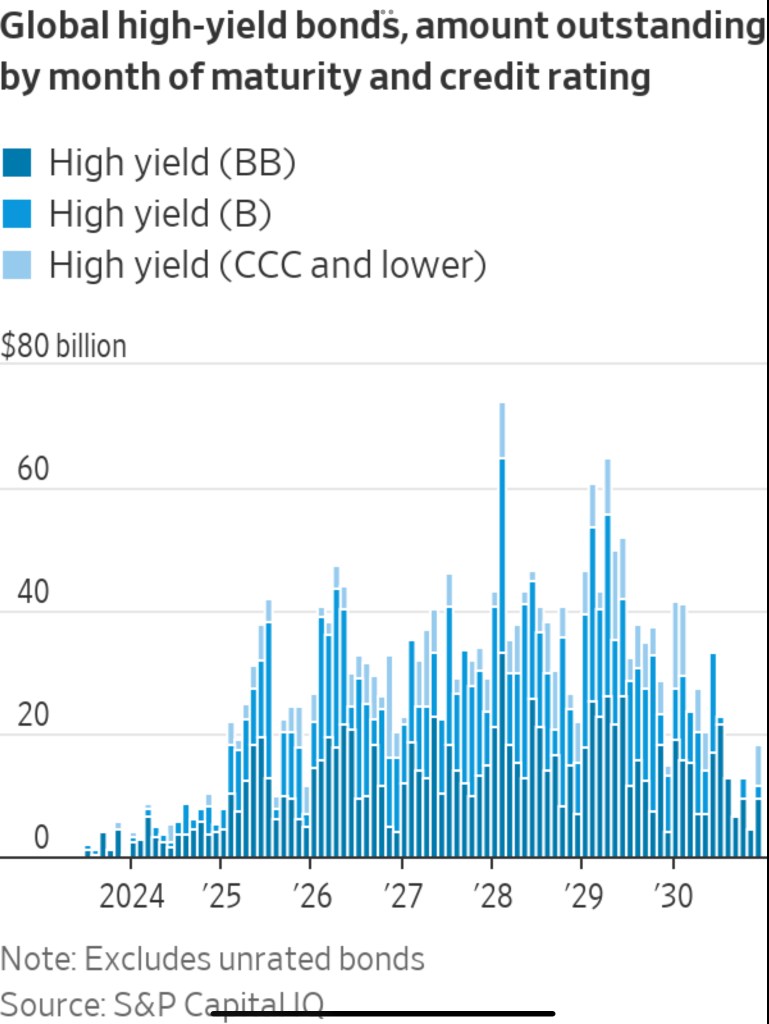

And they have perfect reason to be afraid. The low-rate era of 2021 and 2022 has encouraged private-equity buyouts which increased the amount of risky bonds issued. With the economy remaining unexpectedly strong throughout the first half of the year, investors have been piling into these junk bonds, bonds that have been rated as BB+ or lower with an elevated risk of default, even as interest rates rose. This has led to a boom in junk bond prices. But this also means that these junk bond investors and private equity funds may be in for a bigger reckoning if a recession hits as higher-for-longer interest rates will make financing their bonds more difficult for these problematic companies.

The scale of the looming junk bond crisis is evident in the massive wave of junk bond maturities that begin in early 2025. If a recession begins as expected in late 2023 and lasts for six months, a wave of defaults can be expected. According to David Newman, head of global high yield at Allianz, ratings agencies will start to raise the alarm on junk bonds a year away from their maturity.

If Mr. Newman is correct, then it’s likely that the house of cards in the bond market will start falling in early 2024, because according to S&P Global, junk bonds are usually hit worst when default expectations materially increase. This means that bond investors may be staring down a large wave of defaults that have the potential to worsen the upcoming recession and imperil the ensuing recovery.

This is why the prospect of the Fed tightening further is so dangerous to many. Higher debt financing costs over the longer-term will likely cripple businesses with sagging finances and colossal debt loads, and cause a wave of bankruptcies that the economy has thus far avoided. But with inflation remaining at double the target rate, the Fed will likely remain hawkish in the near run, which means that it may only be a matter of time before the thing hits the fan. In the meantime, anything that could sway the Fed towards dovishness sooner rather than later is a good thing.

Leave a comment